International tourism into South Africa is a pervasive theme which has had a lot of airtime since our borders closed in March this year. It is a massive economic driver and importantly, one which reaches into every economic sector of the country. The informal trader making wire and bead curios, the farmer growing speciality vegetables for a hotel, the international hotel group, the tour bus driver, the mega international airline and the hotel kitchen staff, they are all in it. That’s why it’s important that when we get back to business, we do it right. This is what Sisa Ntshona, SA Tourism ceo has to say:

by Sisa Ntshona

As the world emerges from the economic lockdown brought about by COVID-19, global tourism’s focus is now shifting from crisis management to recovery.

With businesses having experienced a deep and extended disruption, their survival in the local inbound industry depends on their ability to resume operations as soon as it is safe to do so.

The first wave of South Africa’s pandemic has notably eased in recent weeks and the tourism industry has been proactive in establishing and adopting biosecurity protocols to reduce contagion risk across the value chain.

With the restart of domestic tourism, operations are also successfully resuming around the country. As the peak summer season approaches, calls for the reopening of international borders are therefore gathering pace.

Source market travel policy

However, South Africa’s reopening will be driven both by the country’s readiness to receive visitors and by prevailing travel policy in key source markets. While the number of new daily infections is currently far below peak, the rate of infection remains too high for South Africa to yet be placed on the ‘safe travel’ lists.

The United Kingdom provides a pertinent example as one of South Africa’s top three overseas source markets. The UK government has established COVID-19 travel corridors; a list of ‘safe’ countries and territories. Travellers arriving in the UK from countries not on the travel corridor list must self-isolate/quarantine for 14 days. This includes returning UK citizens.

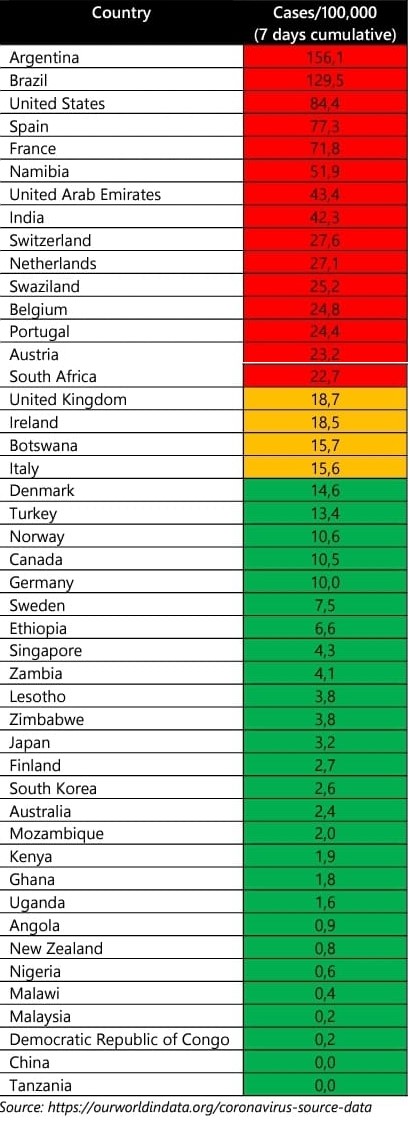

The metric used to assess risk is seven-day cumulative cases per 100 000 people, while other measures such as longer-term case growth, mortality, testing rates and forecast are also considered. The list is currently updated on a daily basis.

Countries are removed from the quarantine-free safe lists when their rise in infections exceeds 20 cases per 100 000 people (the ‘red zone’). Countries with 15-20 cases per 100 000 are classified as amber and those with fewer than 15 cases per 100 000 over seven days are classified as green.

Other European countries such as Scotland, Estonia and Belgium are also implementing ‘safe travel’ or ‘red zone’ lists. On the other hand, Australia has instructed everyone who arrives by sea or air to be quarantined for 14 days with certain exceptions being made for essential travellers only. China has a similar travel policy but has signed fast track agreements with specific countries to support business and essential travel. These countries include Germany, France, South Korea, UK, Japan and Singapore.

Rating South Africa

As of September 7, the seven-day cumulative COVID-19 case count in South Africa was ~13 400. This puts cases per 100 000 people over seven days at 22,7, placing South Africa in the ‘red zone’. Countries classified as red alongside South Africa include Argentina, Brazil, United States, Spain, France, Namibia, United Arab Emirates, India, Switzerland, The Netherlands, Swaziland, Belgium, Portugal and Austria.

For South Africa to drop below 20/100k to the amber zone, the seven-day cumulative COVID-19 case count would need to reduce by about 12%. To drop below 15/100k requires a 34% reduction. Over the last week the seven-day cumulative cases reduced by 12%. If the current trajectory is maintained, South Africa could move through amber and green before the end of the month.

Furthermore, countries in the red zone currently represent just 22% of South Africa’s historic arrivals and 30% of spend. Countries classified as green represent the historic majority of both arrivals and spend. Thus, the majority of the country’s major source markets are already considered ‘safe’ or ‘low-risk’ by the UK classification.

Country readiness

While local operators may be geared to receive international visitors, South Africa is still perceived as being too high risk by its most important markets. It therefore may be premature to consider re-opening borders to international travel as demand is supressed and ‘re-importation’ risk remains acute while South Africa’s own recovery is in its infancy.

The situation is changing rapidly, however, and the trajectory and associated risk rating methodologies inform an approach to target setting. The industry’s booking lead times are material and, if a traveller is to visit the country over the festive period (for example), certainty over their ability to do so is now required. Without this certainty, travellers will choose another destination where such certainty exists.

Using the expected trajectory through red, amber and green risk ratings as a guideline and considering rebound risk, it can be expected that South Africa will once again be perceived as ‘safe’ within the foreseeable future.

In 2019, there were 1,6m arrivals from Europe, which constituted 39% of foreign tourism receipts (spend).